Unit 1 Macro

Economics

January 5, 2016

Macroeconomics- study of the

economy as a whole big picture. (inflation, wage, laws, and international

trade)

Microeconomics- study of the

individual or specific units of the economy. Supply and demand, market

structures, business organization)

Positive economics- attempt

to describe the world as it is. Very descriptive in nature (collects and

protects facts)

Normative economics- attempt

to prescribe how the world should be. (outta, should of) this is opinion based.

Needs- basic requirement for

survival (food, water, shelter, clothing)

Wants- desire but not necessary

Goods- tangible thing

something you can touch

(capitol

goods- items used in creation of other goods such as machinery and trucks

consumer

goods- goods that are intended for

final use by consumer)

services- work that is

perform fundamental problem that all societies face. Trying to satisfy

unlimited wants with limited resources.

Scarcity- most fundamental

problem that all societies face. Trying to satisfy unlimited wants with limited

resources.

Shortage- quantity demanded

is greater than supply

Factor

of production

1.

Land-natural

resource

2.

Labor- work

force

3.

Capitol- human

capitol, physical capitol

4.

Entrepreneurship-

innovative, risk- taker

Resources require to produce goods and services

Human capitol- knowledge, skills, abilities, talents, acquired through education or

experience

Physical capitol- tools, machines, factories, robots, trucks

January 6,2016

Trade-offs-

alternative that we give up whenever we choose one course of action over

another

Opportunity cost- next best alternative ex. Drink get the next best thing cos the place

ran out.

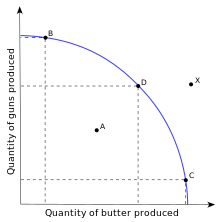

Production possibilities curve- graph that shows alternative ways to use an

economies resources.

4 assumptions of ppg

1.

Two goods

2.

Fixed resources

(land, labor, capitol, entrepreneurship)

3.

Fixed technology

4.

Full employment

of resources

Efficiency- uses resources in such a way as to maximize the

production of goods and services.

Allocative efficiency- the products being produced are the ones that the

society desires

Productive efficiency- products are being produced in the least costly way

and this will represent any point on the ppc or production possibility curve

Underutilization- using fewer resources than an economy is capable of using

3 types of movements within ppg

1.

Inside the ppc-

this occurs when resources are unemployed or underemployed

2.

Along the ppc-

going from B to C or from C to B on the curve

3.

Shifts the ppc-

so if there is an increase in the curve the shift would be D

January 7th

What causes the ppc/ppf to shift?

1.

Advances in

technology

2.

Change in

resources

3.

Change in labor

force

4.

Economic growth

5.

Natural

disasters/ war / famine

6.

More education

on training (human capitol)

January 11, 2016

Demand

Law of demand- the quantities that people are willing and able to

buy at various prices.

Law of demand- occurs when there is an inverse relationship

between price and quantity demanded.

A change in price causes a change in quantity demanded.

What causes a “change”

in demand?

1.

Change in buyers

taste (advertisement)

2.

Change in number

of buyers (population)

3.

Change in price

of related goods

4.

Change in income

5.

Change in

expectations-looking at the future.

Supply

Supply-

the quantities that producers/sellers are willing and able to produce at various prices.

The law of supply- there is a direct relationship between price and quantity supplied.

Change in price causes a “change in quantity supplied”

What causes a “change in supply”?

1.

Change in

expectations

2.

Change in

weather

3.

Change in number

of suppliers

4.

Change in cost

of production

5.

Change in taxes

or subsides

6.

Change in

technology

January 14, 2016

Elasticity of demand- measure of how consumes react to a change in price.

Elastic demand- it is demand that is very sensitive to a change in

price. E>1.

·

Product is not a

necessity.

·

Available

substitutes.

Inelastic demand- demand that is not very sensitive to a change in price. E<1

·

Product is a

necessity

·

Few or no

substitutes

Unit/ unitary elastic- E=1

Elastic demand (Ex. Soda, steaks, candy, fur coats)

Inelastic demand (Ex. Gas, insulin/ medicine, milk, salt, toothpaste)

Price elasticity demand- 3-step formula

|

ELASTIC

|

INELASTIC

|

|

soda

|

gas

|

|

steaks

|

salt

|

|

candy

|

milk

|

|

candy

|

Insulin/

medicine

|

|

Fur

coats

|

toothpaste

|

Step 1:

quantity (new quality-old quantity)

Old quantity

Step 2: price of

item (new price -old price)

Old price

Step 3: PED (%

change in quantity demanded)

% change in price

Cost of production

Total

revenue- the total amount of money a

firm receives from selling goods and services. PxQ=TR

Fixed

cost- a cost that does not change no

matter how much is produced.

Ex.(rent,

mortgage, salaries, insurance)

Variable

cost- a cost that rises or falls

depending upon how much is produced

Ex

(electricity)

Marginal

costs- the costs of producing one

more unit of a good

Formulas-

TFC+TVC=TC

AFC+AVC=ATC

TFC/Q=AFC

TVC/Q=AVC

TC/Q=ATC

TFC=AFC*Q

TVC=AVC*Q

MC=TC-ATC